SOCIAL SHARE

Nov 2, 2025

Leadership and workforce pressures are reshaping the corporate landscape. CEO and CFO turnover is accelerating, executive tenures are shortening, and the labor market is sending mixed signals on job openings, resignations, immigration, and wages. At the same time, artificial intelligence has shifted from optional to essential, bringing both productivity gains and cultural strain.

This is not a temporary cycle; it marks a structural reset in how organizations manage leadership, talent, and resilience. Capital markets are rewarding companies that demonstrate team stability, credible succession plans, adaptable workforce strategies, and thoughtful technology adoption.

Companies that combine succession discipline, workforce agility, and AI integration are best positioned to navigate volatility and maintain investor confidence.

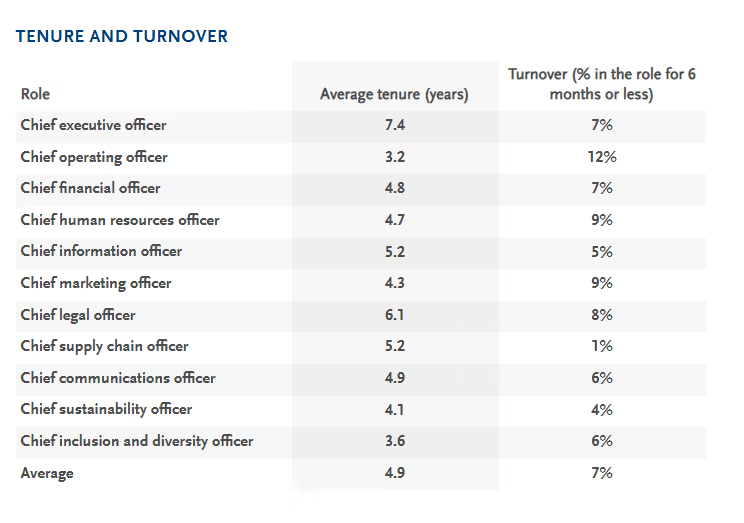

CEO and CFO turnover continues to climb, and shorter tenures are putting greater pressure on boards to prioritize succession planning and leadership readiness. CFOs are particularly vulnerable, with 71%replaced soon after a new CEO takes charge. CEO tenure has dropped below ten years at the largest public companies, with even shorter cycles in private and PE-backed firms.

More than 2,200 U.S. CEOs left their posts in 2024, the highest level in over two decades, up 16% from the prior year, and early 2025 shows no sign of slowing.

Boards are responding with closer oversight, but execution still lags. While many aspire to promote from within, only about half of senior roles are covered by internal pipelines, leaving firms exposed during transitions.2 Poorly managed succession across the S&P 1500 erases nearly $1 trillion in market value each year, while strong processes can lift valuations by as much as 25%.3

Labor market pressures add to the challenge. Rising wages, talent shortages, and immigration shifts are forcing companies to rethink workforce strategies, often prioritizing seasoned operators who can deliver immediate results.4 These dynamics are reshaping decisions about headquarters locations, supply chain design, and overall workforce design.

AI adds another layer of disruption. Early adopters are already achieving measurable productivity and margin gains. Those that delay face inefficiency, stranded costs, and cultural drift. AI is now a defining factor in organizational resilience, not a discretionary choice.

Boards cannot control wage inflation, labor scarcity, or interest rates, but they can control readiness for leadership change. Succession planning has returned to the center of strategic focus. Strong interim playbooks and well-developed leadership benches are critical for smooth transitions. Resilient organizations hold leaders accountable for both performance and talent development.

In the coming quarter, resilience will mean:

Investors are rewarding companies that execute on these fronts, and penalizing those that do not.

1 Spencer Stuart (https://www.spencerstuart.com/research-and-insight/fortune-500-c-suite-snapshot-2024-profiles-in-functional-leadership).

2 DDI’s 2025 HR Insights report (https://media.ddiworld.com/research/ddi-hr-insights-report-2025.pdf?_gl=1*1aj5inz*_gcl_au*MTE3MzYxNjk1Mi4xNzUyMjU1NjE1).

3 2021 Harvard Business Review (https://hbr.org/2021/05/the-high-cost-of-poor-succession-planning).

4 Korn Ferry (https://www.kornferry.com/insights/featured-topics/workforce-management).

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 250 professionals. ZCG is headquartered in New York, with eight affiliated offices, across six countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

ZCG Consulting (“ZCGC”) is the business consulting platform of ZCG and is a results‐oriented management consulting firm for middle market businesses. A reliable resource for private equity firms and their portfolio companies, our professionals offer deep functional expertise and customizable hands-on solutions to accelerate growth.