Key Takeaways – Navigating Credit Cycles with an Information Edge

Default activity is quietly picking up

September saw the highest default volume of the year, lifting the leveraged-loan default rate to 3.5% (1). While headline figures remain contained, the growing use of coercive exchanges and PIK structures is concealing deeper balance-sheet stress.

Too much capital, too few opportunities

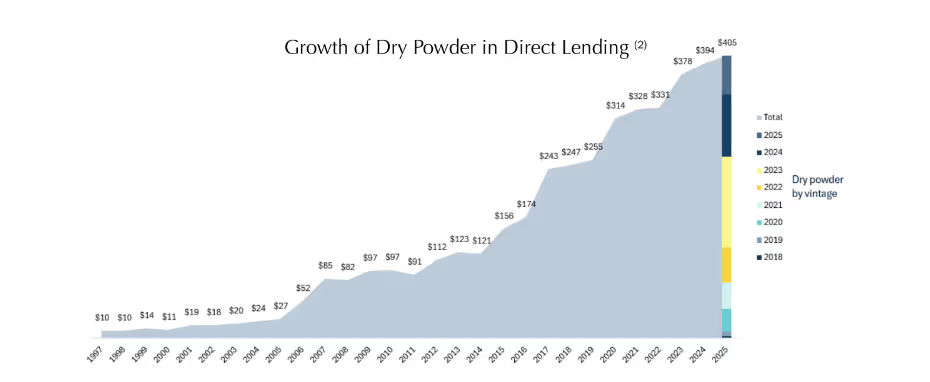

Over two-thirds of the $400 billion in U.S. direct-lending dry powder has been raised since 2023(2). As a result, managers are facing mounting pressure to deploy. This imbalance–too much capital chasing too few opportunities–has kept spreads near multi-year lows despite rising leverage and deteriorating credit quality.

Technology is redefining how credit investors identify and manage risk

Advantage now lies in how quickly raw data can be transformed into insight. Connecting public, private, and alternative data sources allows investors to spot inflection points before the market reacts.

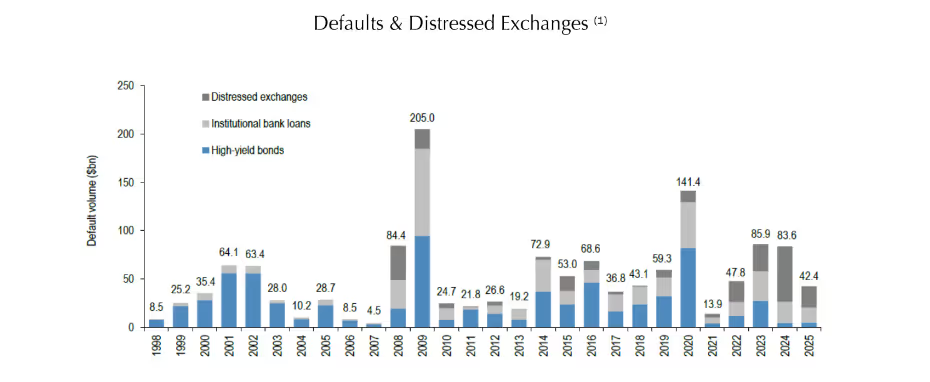

Defaults Rising Beneath the Surface

After a muted first half, default activity began to normalize in the third quarter. Total defaults and distressed exchanges reached $5.4 billion in leveraged loans during September, the highest monthly level since 2023. So far in 2025, more than forty companies have defaulted or completed exchanges totaling $42 billion in affected debt.

Distressed exchanges and liability management exercises (LMEs) are on pace for the third-largest annual total on record, accounting for 51% of year-to-date (YTD) total default / distressed exchange volume–significantly elevated relative to long-term average of 22% (1).

Borrowers are increasingly relying on amendments, maturity extensions, and PIK interest in delaying problems rather than resolving them. As a result, default statistics have become lagging and incomplete indicators. Many credits that appear to be “performing” are, already reliant on structural relief to remain current.

Liquidity Masking Weak Fundamentals

Excess liquidity continues to mask underlying weaknesses in the leveraged-loan market.

Estimated direct-lending dry powder now exceeds $400 billion, with more than two-thirds raised in the past two years. Meanwhile, CLO issuances are up roughly 20% year-over-year through September.

Together, these forces have created an overcapitalized ecosystem in which direct lenders and CLOs compete for the same investment opportunities. This surge of capital has driven spreads to multi-year lows–compressing leveraged-loan spreads to around 450 bps, down from over 600 bps in 2022–even as credit quality has eroded.

The abundance of liquidity has also blurred traditional sources of differentiation. Most credit managers today are pursuing similar sponsor-led opportunities and comparable terms. The ability to “cherry-pick” transactions or align with top sponsors is no longer a defining advantage.

As a result, alpha generation is shifting from access to insight–from sourcing deals to interpreting data. The leading managers are those able to detect inflection points in borrowers’ financial health through systematic pattern recognition, contextual analysis, and continuous data monitoring.

Technology as an Extension of Fundamental Credit Work

Credit investing remains grounded in fundamentals, but the speed and complexity of information flow have increased exponentially.

Quarterly updates and management calls are no longer sufficient to keep pace with real-time market dynamics. Credit managers now need live data to enhance decision-making and identify portfolio risks earlier. This data-driven approach has several practical applications:

- Macro and market context: Continuous monitoring of macroeconomic indicators and public-company data helps detect divergences between market trends and company-specific performance. Comparing metrics such as revenue growth, margins, and customer trends can reveal when a borrower’s fundamentals diverge from industry norms–an early signal of emerging risk or relative strength.

- Alternative data integration: Non-traditional datasets–including job postings, web traffic, and credit-card transaction–offer real-time insights into business activity. These indicators provide an early view of demand shifts, customer behavior, and operational health, especially in consumer-facing sectors.

- Cross-company benchmarking: Private-company data can be benchmarked against a proprietary database of historical issuers to identify anomalies in leverage, liquidity, or profitability. Deviations from established cohorts often precede stress, enabling earlier detection and prioritization by credit analysts.

- Automated portfolio surveillance: Integrating all these inputs enables monitoring systems to flag early signs of deterioration well before they appear in financial reports or market pricing.

Turning Data into Edge

A decade ago, differentiation in credit came from origination networks and sponsor relationships. Today, it comes from how information is captured, analyzed, and applied.

When data and judgment are integrated across underwriting and portfolio management through technology, the investment process becomes more informed and adaptive. Over time, that creates a differentiated edge by enabling credit managers to translate information into action.

While technology will never replace fundamental underwriting, it has become indispensable tool. It enables credit managers to identify performance shifts early, act decisively, and ultimately enhance both risk management and returns.

Sources

1 JP Morgan Default Monitor dated October 1, 2025

2 Pitchbook Q1 2025 US Debt Capital Overhang Report

3 CS Leveraged Loan Index

About

ZCG

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 250 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.