.png)

SOCIAL SHARE

Apr 27, 2026

ZCGC Insights: It's All About the Box – How Location, Data, and Execution Are Defining Multi-Site Performance

%20(2).jpg)

Multi-site businesses are operating under a fundamentally different set of conditions than the ones that governed the last decade of expansion. Capital is more expensive, consumers are more selective, and the cost structure has reset higher. What used to be cyclical pressure has become structural, and the math of value creation has shifted accordingly.

Returns are now earned at the asset level, one box at a time.

Several external forces are compounding this pressure:

Performance is no longer driven by brand strength alone. It is determined by whether each individual location, the box, can sustain and adapt within its specific market.

Two casual dining chains operating in the same segment, under similar consumer conditions, have recently produced starkly different results.

Chili's posted approximately +31% same-store sales growth in a single quarter, driven by value-focused marketing and a disciplined, multi-quarter turnaround. (5)

Applebee's, in the same segment, has reported seven consecutive quarters of same-store sales declines and is closing units and co-branding locations to mitigate underperformance. (2)

Two brands. Same consumer. Same segment. Opposite outcomes.

The difference is not brand equity. It is execution at the unit level, pricing, traffic, store condition, staffing, and site-by-site performance management. This pattern is now evident across all multi-site categories, from restaurants and fitness to hospitality and retail. Brand strength sets the ceiling. The box determines whether the operator gets there.

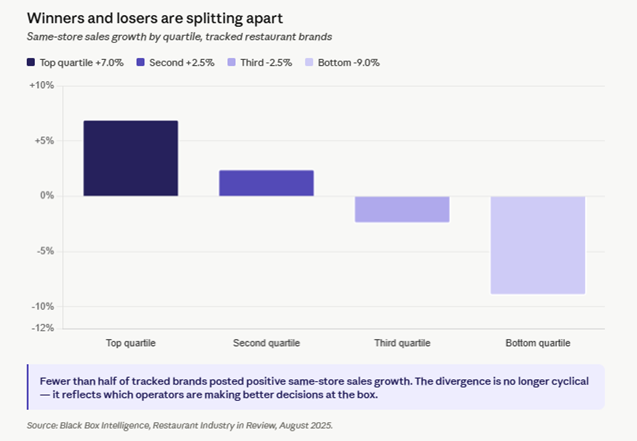

Four-bar chart showing top quartile (strong positive growth), second quartile (modestly positive), third quartile (modestly negative), bottom quartile (sharply negative). Fewer than half of tracked brands posted positive same-store sales growth(3):

Industry-level same-store sales growth has remained positive in recent months, but fewer than half of tracked brands have participated. The bottom quartile continues to underperform sharply, while top performers gain share.

Divergence is no longer cyclical; it reflects which operators are making better decisions at the box.(3)

Most multi-site portfolios were built in a period when speed and scale were rewarded, and expansion decisions were made on broker narratives and static demographic overlays. That approach now produces three consistent patterns:

In an environment where every point of EBITDA growth must be earned, these inefficiencies are no longer absorbable.

Across ZCGC engagements, top-performing operators and sponsors producing consistently demonstrate four core disciplines:

For multi-site operators and their sponsors, real estate is no longer a passive input, it is the operating system that governs capital deployment and return generation.

ZCGC works across the full lifecycle of the box, integrating data-driven site selection, lease structuring, development execution, and portfolio optimization into a single operator-led framework: real estate, operations, talent, and finance decisions made in alignment, by the same team, against the same plan.

The strategy can be sound. The brand can be strong. But in multi-site businesses, the outcomes are determined at the box.

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

ZCG Consulting (“ZCGC”) is the business consulting platform of ZCG and is a results‐oriented management consulting firm for middle market businesses. A reliable resource for private equity firms and their portfolio companies, our professionals offer deep functional expertise and customizable hands-on solutions to accelerate growth.

.png)