SOCIAL SHARE

May 1, 2025

ZCG Credit Insights: Navigating Tariff-Driven Uncertainty in Credit

Recent tariff announcements have introduced substantial uncertainty in the leveraged credit markets, significantly impacting sentiment and likely prompting borrowers to pursue proactive liability management strategies.

The new tariff regime poses a threat of material margin compression, intensifying liquidity stresses for borrowers with weaker balance sheets and lower credit quality.

Continued erosion of covenant protections is facilitating the rise of uptiering and drop-down financings across credit markets.

In early April 2025, market volatility surged following President Trump's announcement of sweeping tariff increases. While a temporary 90-day negotiation period has since been introduced to review and possibly adjusts the proposals, the uncertainty continues to weigh heavily on market and investor sentiments.

Wall Street economists have revised their U.S. recession forecasts upward in response, warning that these tariff policies could significantly impair global economic growth and push the U.S. economy closer to recession territory.

The initial proposal suggested an effective U.S. tariff rate approaching 23%,equivalent to a sizable tax increase on imports, substantially disrupting global trade flows and inflation dynamics. Even after the temporary moderation, economists still expect a sustained average tariff rate of approximately 16%, representing a significant shock to both corporate margins and GDP growth.

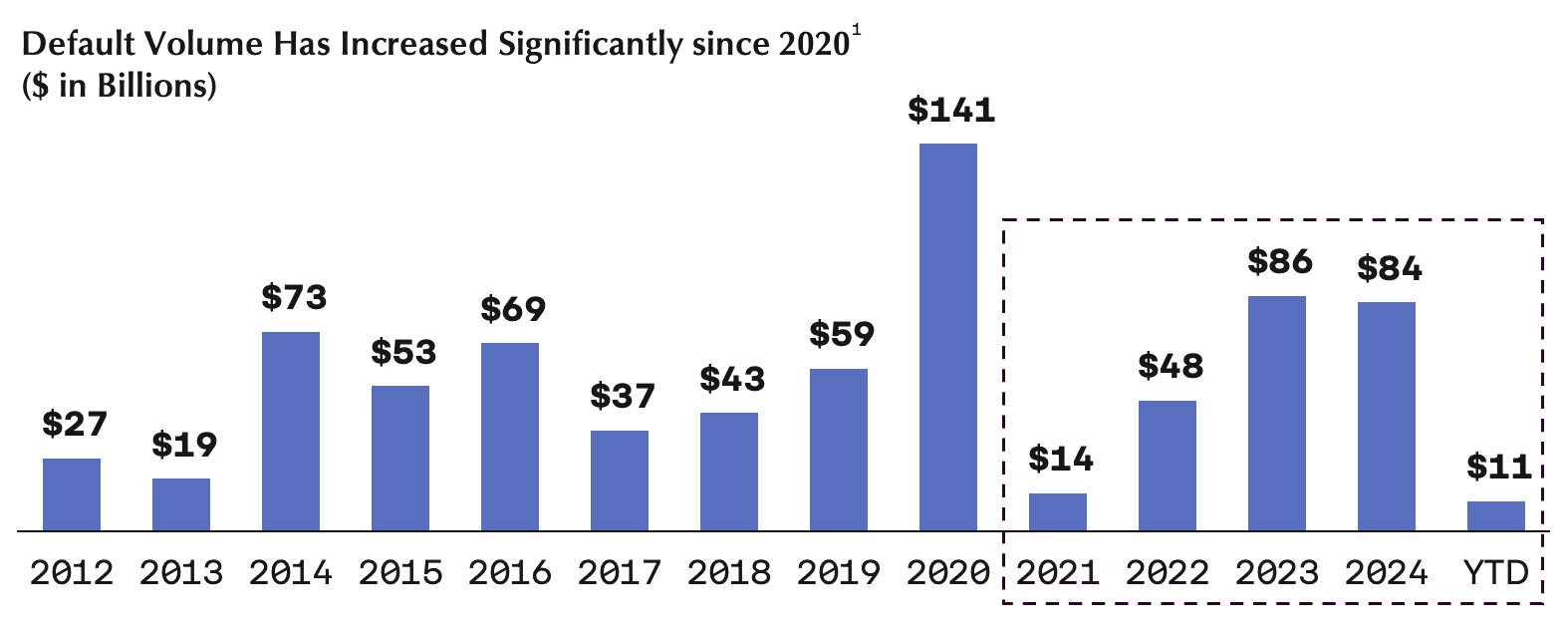

Even prior to the April 2025 announcements, LME activity had been increasing steadily since 2020, reaching record levels in 2024 and continuing through Q12025. According to Covenant Review, at least 17 new LME transactions occurred in the first quarter alone, many involving uptiering and superpriority components.

Although legal developments such as the Serta Simmons decision were expected to curb these practices, LME strategies remain widely used—reflecting their strategic utility in times of financial distress.

With tariffs heightening economic and operational risks, borrowers are increasingly turning to LMEs as a mechanism to manage liquidity and restructure obligations. We anticipate further upticks in liability management activities through the remainder of 2025.

According to the International Monetary Fund (IMF), over 40% of private credit borrowers had negative free cash flow (FCF) by the end of 2024, a sharp rise from approximately 25% in 2021. This deterioration heightens default risk, particularly in sectors like healthcare and software, where idiosyncratic vulnerabilitiesare common.

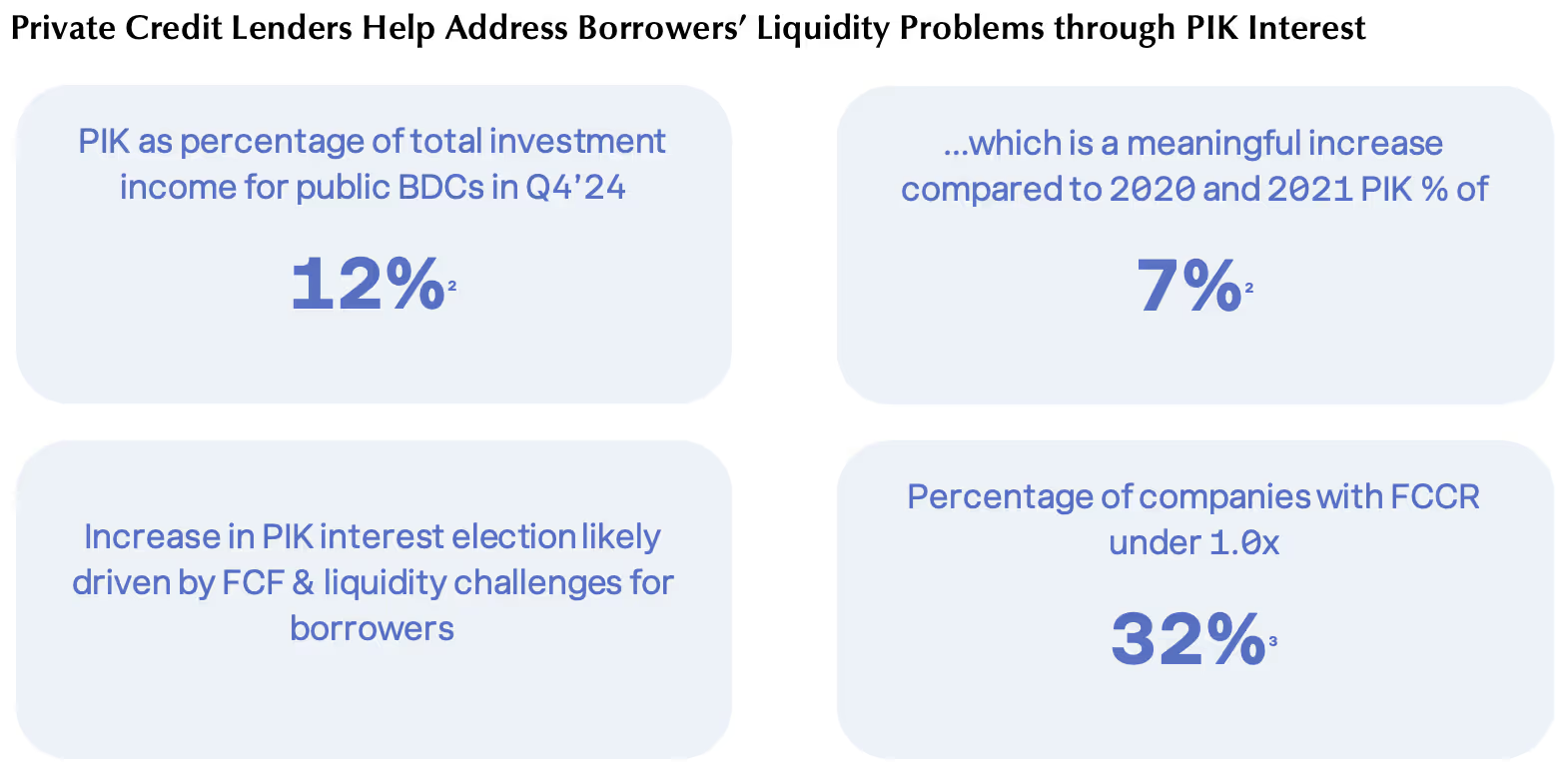

Borrowers’ growing reliance on Payment-In-Kind (PIK) interest structures—now representing over12% of investment income for publicly traded BDCs as of Q4 20242 —reflects widespread liquidity constraints. While PIK provides temporary cash flow relief, it often masks underlying financial weaknesses and is not sustainable long-term.

Given that the $1.6 trillion private credit market is more exposed to smaller, undercapitalized borrowers than the broadly syndicated loan (BSL) market, the current economic climate places it under pronounced strain. Tariff-induced costinflation and supply chain disruptions are compounding existing pressures. The IMF has also warned that the deterioration in borrower credit quality is notyet fully reflected in accounting valuations, raising concerns over hidden risks within portfolios.

The confluence of negative cash flows, reliance on PIK, and aggressive financial engineering highlights the fragile position of many private credit borrowers in this environment.

Covenant Review continues to track a weakening trend in borrower covenants across the leveraged loan markets. High-profile structural loopholes—such as J. Crew-style asset transfers and Serta-style non-pro rata amendments—remain prevalent.

Currently, approximately 35% of loans permit majority consent voting structures (facilitatingthe "Serta loophole"), and around 45% permit IP transfers tounrestricted subsidiaries (enabling the "J. Crew Loophole")4.

As borrowers face sustained operational and financial stress, we expect continued growth in LMEs exploiting these structural flexibilities. In this environment, disciplined credit selection, proactive portfolio surveillance, and early restructuring engagement will be essential tools for credit investors.

1 J.P. Morgan report – “Credit Strategy Weekly Update” (April 4, 2025)

2 Bloomberg research & company filings

3 Lincoln International Capital Advisory Market Update (December 2024)

4 Covenant Review – Private Credit Special Report (February 28, 2025)

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

.png)

.png)