SOCIAL SHARE

Jul 1, 2025

ZCG Credit Insights: The "True" Distress Level in Private Credit

The rise of covenant-lite structures has enabled borrowers to engineer amendments and extensions that avoid triggering defaults– effectively masking financial stress.

These tools preserve optics at the expense of long-term borrower viability, leaving fundamental challenges unresolved.

Unresolved trade headwinds are compounding financial strain. We expect a broader wave of distress to emerge in the second half of 2025.

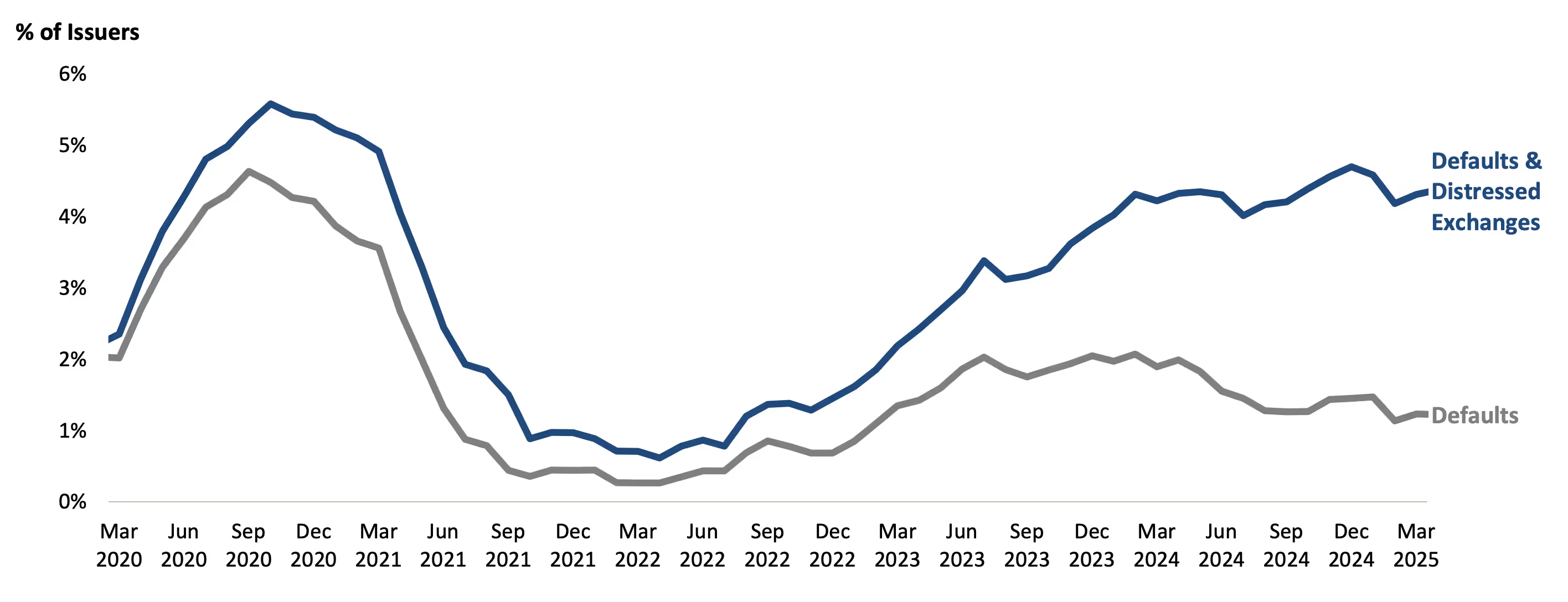

On paper, credit markets appear healthy. As of Q1 2025, only 1.2% of broadly syndicated loan (BSL)issuers are in default and publicly traded BDCs show a non-accrual rate of approximately 3%(1)—not alarming by historical standards.

However, beneath stable headline numbers, borrower fragility is increasing.

PIK interest now accounts for over 8%(1) of total income across BDCs—double the pre-COVID level—signaling growing liquidity stress. Meanwhile, forbearances, maturity extensions, and waiver-heavy amendments have become widespread. Covenant-lite structures have facilitated these practices, allowing borrowers to sidestep defaults despite declining financial performance.

In many cases, a loan’s “performing” status reflects leniency rather than actual credit health.

The gap between traditional default rates and those including distressed exchanges has widened, further obscuring the true level of market distress.

Defaults Alone Don’t Tell the Full Story(2)

Distress indirect lending isn’t just increasing—it’s becoming harder to detect. Borrowers may appear current on paper, but structural signals suggest growing impairment.

According to Lincoln International’s Q1 2025 data(3), direct lending loans are still marked at 98.7% of par—down only 0.1% since Q4 2024—and average EV multiples remain above 11.7x.

These figures are difficult to reconcile with rising input costs, slowing revenue growth, and shrinking exit optionality. The result: artificially smooth marks that obscure real-time deterioration.

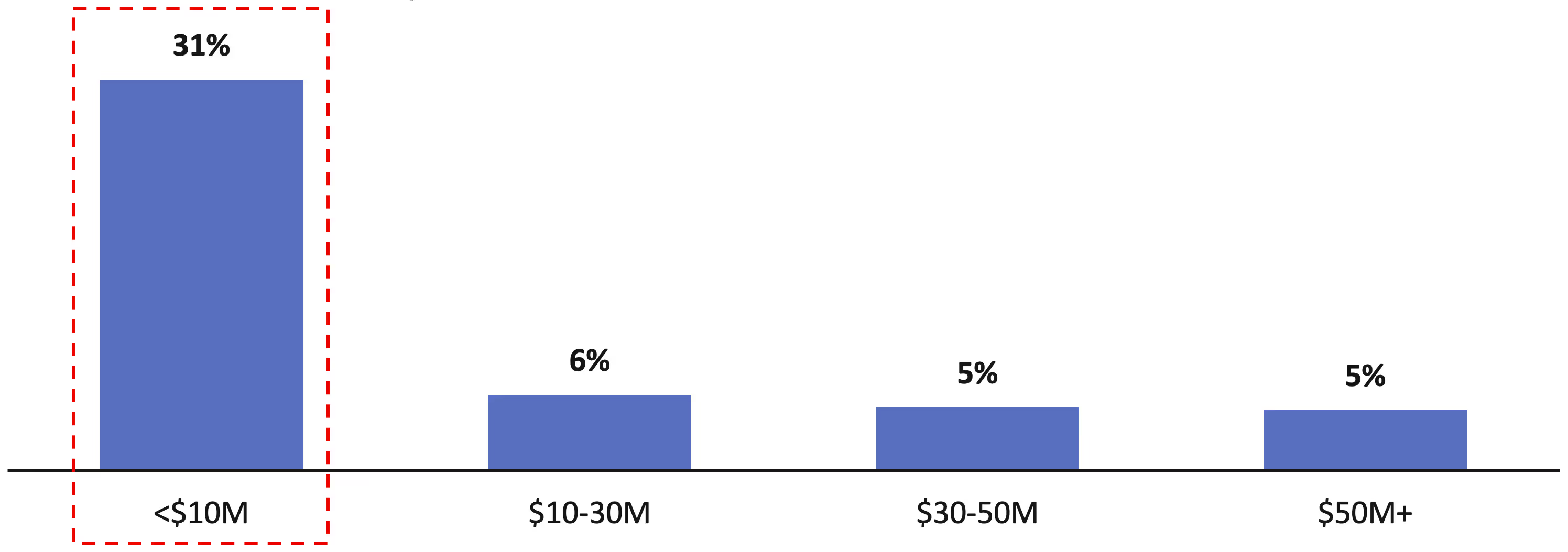

Stress is particularly concentrated in the lower middle market. Borrowers with less than $10 million in EBITDA now show covenant default rates above 31%, while larger companies remain more insulated.

Covenant Default Rates by Borrower EBITDA Size(3)

This size dispersion is critical for LPs with exposure to sponsor-led middle-market direct lending platforms. Exit options have also narrowed. M&A volume remains muted, IPO markets are closed, and refinancing avenues are increasingly constrained—leaving more borrowers with liquidity shortfalls and few viable paths.

While headline default activity may remain contained, we anticipate a sharp increase in below-the-surface credit events, particularly:

1 Bloomberg & company filings of 14 BDCs tracked by ZCG Credit for illustrative purposes to provide broad market commentary

2 JP Morgan – US Leveraged Loan Default Rates

3 Lincoln Private Market Perspective Q1 2025

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

.png)

.png)