SOCIAL SHARE

Jan 23, 2025

ZCG Credit Insights: Rough Road Ahead for Direct Lending

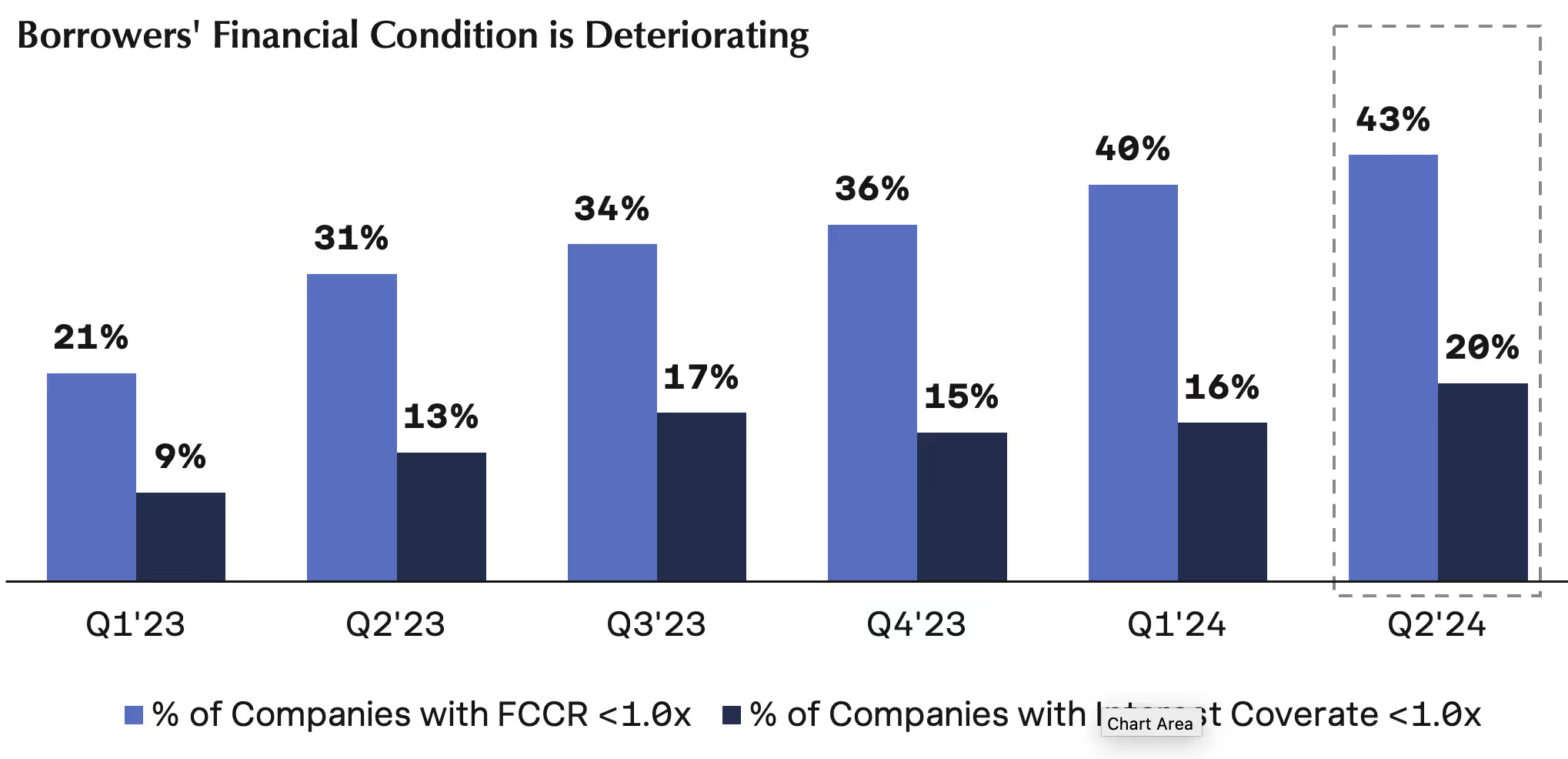

While excess dry powder has intensified competition among direct lenders, the underlying credit quality of borrowers has been deteriorating, with over 40% of private companies now facing debt service costs exceeding their free cash flow, according to a recent report from Lincoln International.

The era of easy returns in the private credit sector appears to be ending, as increased competition has ushered in a period of lower spread premiums over more liquid loans.

Despite the surge in direct lending volume, approximately 50% of direct lending funds raised since 2021 remain undeployed as of November 2024, suggesting that spread compression will likely persist.

The private credit market has grown almost 10x since 2009, standing today at approximately $1.7 trillion1. The asset class performance benefited significantly from the Federal Reserve’s tightening monetary policy, which brought in a large supply of new investor interest. A recent report fromMorgan Stanley estimates the asset class could grow to $2.8 trillion by 20282. However, demand for credit has lagged supply, and with signs of deterioration emerging in underlying fundamentals, rigorous credit selection will be an essential driver of future performance.

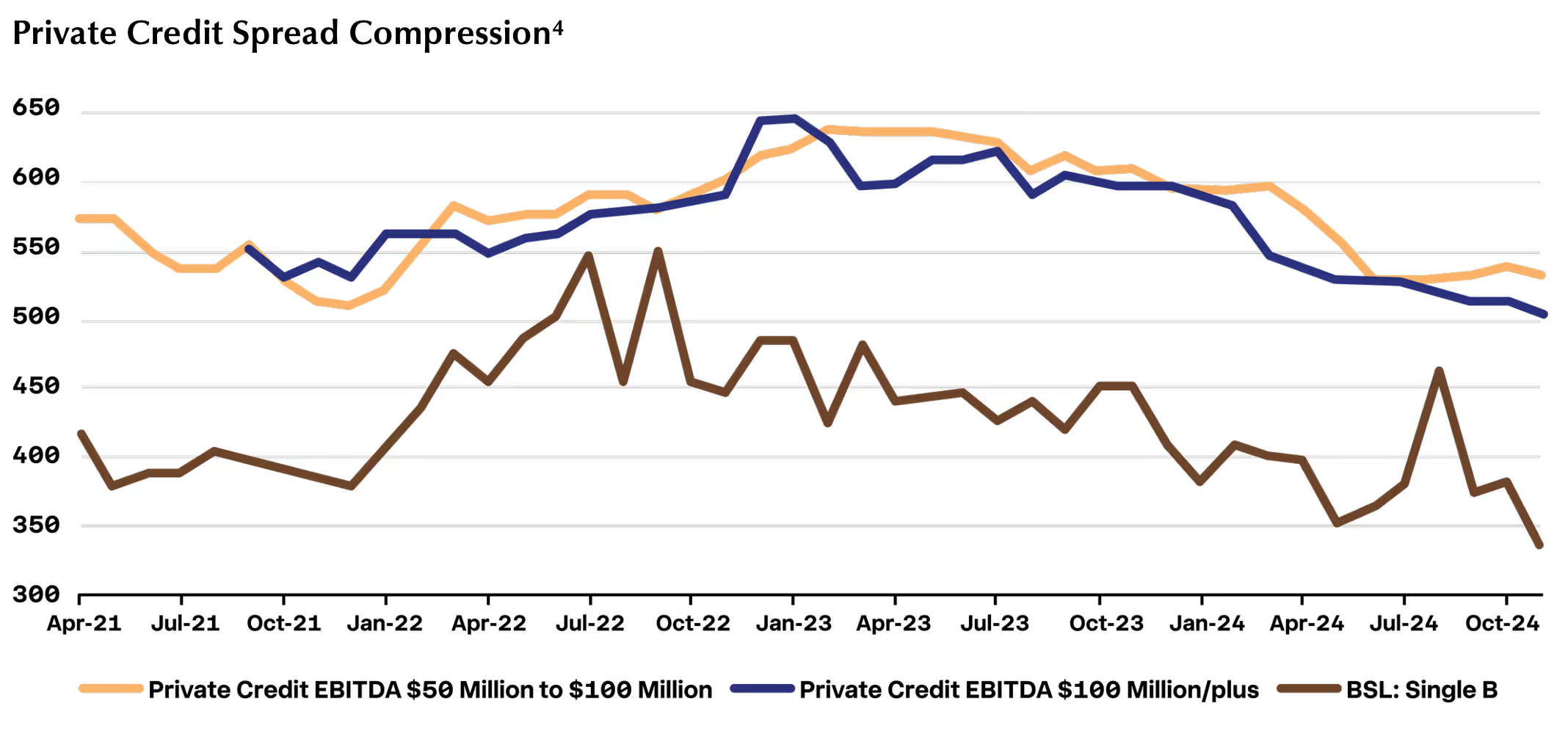

As direct lending assets under management have increased, competition has intensified, and leveraged credit markets saw significant refinancing activity in 2024. According to data compiled by Configure Partners3, refinancings outpaced LBO andM&A financings by roughly 50% in 2024. This has led to a nearly 150bps compression in spreads over the last two years, eroding the liquidity premiums traditionally associated with the private credit market. Our conversations with private equity firms reveal an extremely competitive lending landscape with firms receiving 20-30 term sheets for each financing opportunity in this borrower-friendly environment, leading us to believe that the winner on these financings might be the loser.

Borrowers are now negotiating aggressively on documentation, resulting in weaker credit agreements and more relaxed covenant packages, historically a strong point of differentiation for private credit versus the broadly syndicated market.

“The underlying credit quality of borrowers has been deteriorating, with over 40% of private companies facing debt service cost that exceeds their free cash flow.”

Shahid Khoja

Managing Director, Head of Credit

While excess dry powder has intensified competition among direct lenders, the underlying credit quality of borrowers has been deteriorating, with over 40% of private companies facing debt service cost that exceeds their free cash flow according to a recent report from Lincoln International5. This trend is also evident when looking at average non-accrual rates for public Business Development Companies(BDCs), which have crept up steadily from 3.72% in 2Q23 to 4.09% in 2Q246.Additionally, average payment-in-kind (PIK) income as a percentage of net investment income has risen to 20% in Q2’24 from 12% in 20217. While not all PIK debt is inherently problematic, it is likely that direct lenders and borrowers are employing short-term measures, such as converting to payment-in-kind and amend & extend transactions, to alleviate immediate pressures – solutions that we believe are unsustainable in the long term.

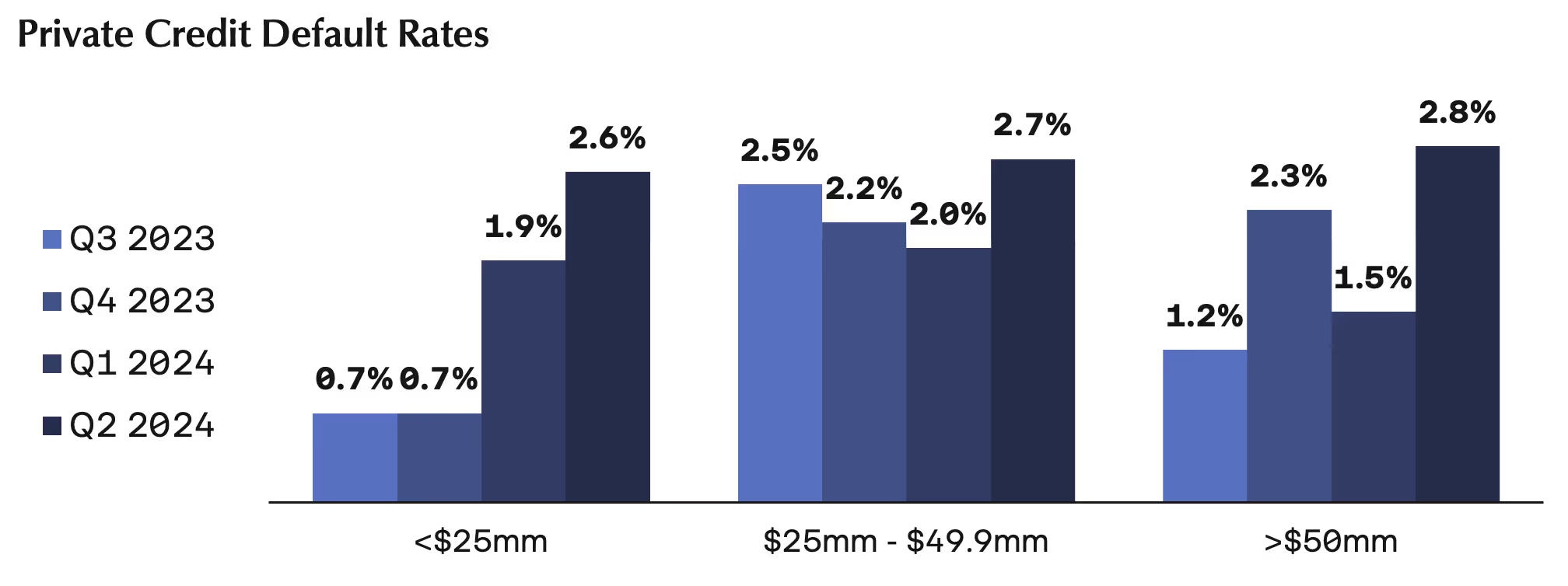

Defaults have already begun to rise across borrowers of all sizes, as indicated by the Proskauer Private Credit Default Index8. According to Fitch Ratings9, the largest driver of defaults is the introduction of PIK or a deferral of one more interest payment, with maturity extensions accounting for a smaller portion of the increase. However, with base rates remaining elevated following a slew of macroeconomic data, the likelihood of this persisting for longer than expected is a real risk that investors must account for when analyzing the private credit market.

The era of easy returns in the private credit sector is showing signs of waning, and increased competition is ushering in a period of lower spread premiums over more liquid loans. Despite the surge in direct lending volume, approximately 50% of direct lending funds raised since 2021 remain undeployed as of November 202410, indicating spread compression is likely to persist. The market now expects fewer interest rate cuts in 2025 due to renewed inflationary pressures. This environment of prolonged high rates signals additional credit risk that in our view needs to be accounted for when comparing opportunities across the asset classes.

With lower ‘illiquidity premium’ providing less cushion, rigorous credit analysis and thoughtful portfolio construction are vital for futureperformance. We continue to monitor market dynamics closely and remain committed to our disciplined investment approach.

1 Morgan Stanley Private Credit Tracker (as of July 29, 2024)

2 Morgan Stanley report – “Understanding Private Credit” (June 20, 2024)

3 9Fin report – “The Unicrunch – Private credit spreads continue to tighten” (October 10, 2024)

4 KBRA Report – “Private Credit: 2025 Outlook” (January 14, 2025)

5 Lincoln International Capital Advisory Market Update (August 2024)

6 Public filings of BDCs / JPM Credit Watch Report – “Private Credit Uncovered – Just the Two of Us, We Can Make It Underwrite” (October 8, 2024)

7 Public filings of BDCs / JPM Credit Watch Report – “Private Credit Uncovered – Just the Two of Us, We Can Make It Underwrite” (October 8, 2024)

8 Proskauer report – “Private Credit Defaults Rise to 2.71% According to Latest Proskauer Index” (July 22, 2024)

9 Fitch Ratings report – “U.S. Private Credit Default Rate Debuts at 5.0% for August 2024” (September 25, 2024)

10 Data from Preqin (an unaffiliated third-party alternative assets benchmarking firm)

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

.png)

.png)