.jpg)

SOCIAL SHARE

Feb 23, 2026

ZCGC Insights: Tariff Disruption: IEEPA Tariff Ruling — FAQs and Immediate Action Steps for Importers

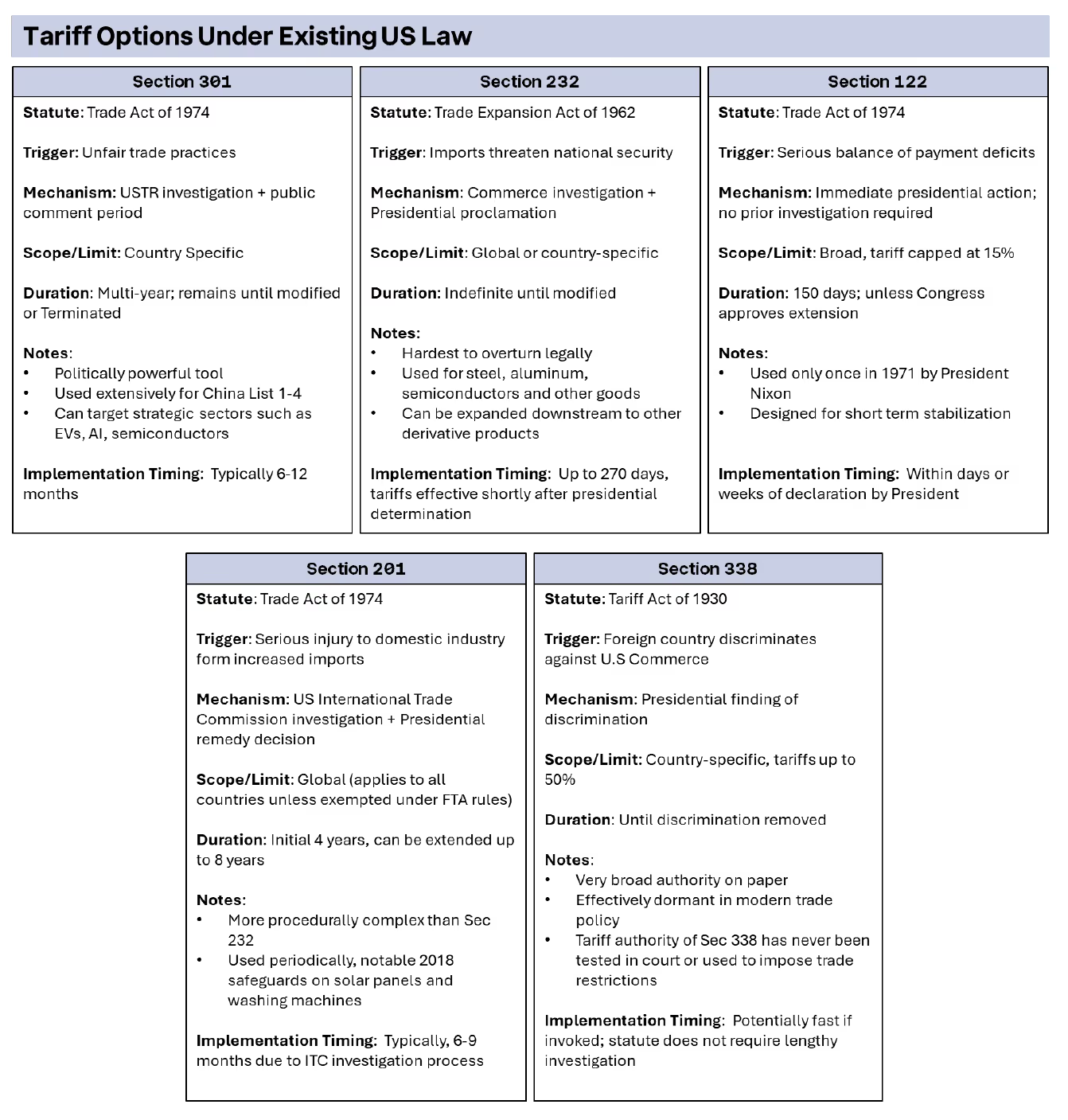

The recent Supreme Court ruling struck down certain tariffs imposed under IEEPA authority. While the decision is narrowly focused and does not affect longstanding programs such as Sections 301, 232, or 201, it materially alters the legal foundation for a portion of recent duties.

The result is a rapidly evolving environment. Companies must now assess potential refund eligibility, monitor possible reissuance of tariffs under alternative statutory authorities, prepare for litigation pathways, and manage short-term supply chain and pricing disruption.

The decision removed the legal basis for certain tariffs imposed under IEEPA authority only. It did not affect Section 301, Section 232, AD/CVD, or normal MFN duties. The ruling addressed the legality of the IEEPA tariffs exclusively. The Court did not issue guidance regarding refund mechanics.

The ruling did not address refund procedures. It is expected that importers willneed to file Post-Summary Corrections for unliquidated entries, protests for entries liquidated within the 180-day statutory window, and potentially pursue litigation at the Court of International Trade for older entries outside the protest period. Until additional guidance is provided by the Court of International Trade or CBP, uncertainty will remain.

The administration invoked Section 122 within hours of the ruling,which permits a temporary tariff of up to 15 percent for 150 days under abalance of payments justification. That tariff is scheduled to take effect on February 24. Other statutory authorities remain available for tariff implementation, including Sections 232, 301, 201, 122, and 338.

CBP issued operational guidance advising that collection of the affected IEEPA tariffs will cease at 12:00 a.m. on February 24.

Tariffs may pause, return under different statutory authority, and then face further legal challenges. The operating environment over the coming months is likely to remain volatile.

Additional legal challenges are highly likely. Sections 301, 232, and 201 are less likely to face successful challenges because their procedural frameworks have been established and used for years. By contrast, Section 338 has never been used to impose tariffs, and Section 122 has only been used once. Section 122 is intended for a “serious balance of payments emergency,” and characterizing longstanding trade deficits as such may invite legal scrutiny.

There is ongoing uncertainty regarding how this ruling may interact with recently negotiated trade agreements or pending tariff actions. For example, the European Union has reportedly paused further discussions on a potential U.S.–EU trade agreement pending greater clarity on U.S. tariff authority.

Tax implications may also arise depending on how duties were previously accounted for, including potential income recognition and inventory valuation adjustments.

Statutory interest should accrue on overpaid duties. For larger importers, the interest component could become meaningful over time.

Refund claims will likely trigger documentation review. Companies should expect information requests and potential post-entry audits. Clean, entry-level documentation will be critical to support successful recovery efforts.

Importers should move quickly to get organized. The first step is to pull ACE data and identify the full universe of affected entries. Entries should then be segmented by liquidation status, and duty payments reconciled toensure accuracy. Customs brokers should be engaged early to confirm that documentation is complete, consistent, and audit-ready.

Given the volume of formal entries filed annually, both brokers and CBP are likely to face operational strain. Execution discipline will be a key differentiator in determining which companies successfully recover funds andhow quickly those recoveries occur.

Supreme Court Ruling: 24-1287Learning Resources, Inc. v. Trump (02/20/2026)

White House Executive Order: Ending Certain Tariff Actions(2/20/2026)

Cargo Systems Messaging Services (CSMS) #67834313

United States, Congress. International Emergency EconomicPowers Act. 50 U.S.C. §§ 1701–1707

United States, Congress. Trade Act of 1974, Section 301.19 U.S.C. § 2411

United States, Congress. Trade Expansion Act of 1962,Section 232. 19 U.S.C. § 1862

United States, Congress. Trade Act of 1974, Section 201.19 U.S.C. § 2251

United States, Congress. Trade Act of 1974, Section 122.19 U.S.C. § 2132

United States, Congress. Tariff Act of 1930, Section 338.19 U.S.C. § 1338

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

ZCG Consulting (“ZCGC”) is the business consulting platform of ZCG and is a results‐oriented management consulting firm for middle market businesses. A reliable resource for private equity firms and their portfolio companies, our professionals offer deep functional expertise and customizable hands-on solutions to accelerate growth.

.png)

.png)