.jpg)

SOCIAL SHARE

Mar 5, 2026

As 2026 unfolds, the operating environment has settled into a new reality. Higher capital costs, sustained margin pressure, and elevated execution risk are no longer temporary disruptions – they are structural features of the landscape. While conditions have stabilized relative to prior years, the margin for error remains narrow, and the firms that thrive will be those that treat balance-sheet discipline as a strategic advantage, not a defensive posture.

In response, the most effective operators are treating the balance sheet as a strategic control mechanism and not a static financial outcome. Fixed obligations, lease exposure, working capital, and long-dated contractual commitments are now being actively managed in lockstep with day-to-day operating decisions.

The firms navigating this environment most effectively are not relying on siloed advisors or isolated initiatives. Instead, they are adopting integrated, operator-led approaches that align real estate, supply chain, talent, and finance decisions into a single execution framework. This coordination, which is rare among traditional advisory models, has emerged as the critical competitive advantage, and it is the foundation of ZCGC’s approach to every engagement.

Recent quarters have reinforced how balance-sheet structure now directly determines operating flexibility.

Many organizations continue to address balance-sheet pressure through fragmented advisory approaches. Real estate, restructuring, supply chain, and talent decisions are often evaluated independently, despite being operationally interconnected. In practice, this means a company may renegotiate a lease portfolio without understanding its impact on workforce planning, or restructure vendor contracts without modeling the working capital consequences.

This siloed model consistently creates three challenges:

In volatile environments, fragmentation increases risk rather than mitigating it.

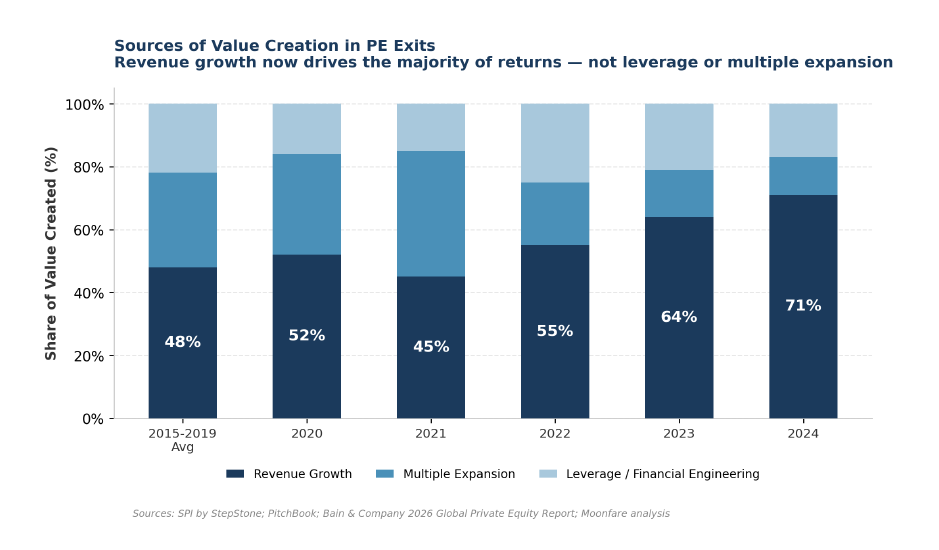

According to Bain & Company’s 2026 Global Private Equity Report, revenue growth accounted for 71% of value created in 2024 exits, up from 64% in 2023, confirming that operational improvement has displaced financial engineering as the primary driver of returns. Yet fragmented advisory models remain the norm, leaving most firms unable to execute on this shift. (1)

While many firms remain reactive, the most effective operators are deploying integrated, execution-driven strategies. Across ZCGC engagements, four themes consistently define success:

• Integrated Balance-Sheet Governance: Balance-sheet implications are evaluated upfront through coordinated decision-making across real estate, capex, labor, and liquidity, rather than addressed after execution.

• Active Management of Fixed Obligations: Leases, vendor contracts, and long-term commitments are treated as dynamic financial instruments, with focus on duration, escalation, exit optionality, and risk transfer.

• Working Capital Embedded in Operations: Inventory positioning, procurement terms, and liquidity planning are directly aligned with operating forecasts, improving cash conversion and reducing surprise risk.

• Operator-Led Execution: Rather than relying on siloed advisors, leading firms deploy cross-functional teams that integrate real estate, supply chain, talent, and finance expertise into a single execution plan.

In 2026, balance-sheet performance is no longer driven by finance alone. It is shaped by operational decisions and the degree to which those decisions are coordinated across the enterprise.

ZCGC works alongside management teams to align real estate strategy, working capital discipline, organizational design, and capital planning into a unified execution framework. This integrated approach allows companies to reshape balance-sheet exposure, unlock liquidity, and preserve flexibility without relying on reactive restructuring or external capital.

As volatility becomes a permanent feature of the operating environment, balance sheets will remain the primary battleground for value preservation and creation. Firms that outperform will be those that act decisively, actively manage obligations, and replace fragmented advisory models with integrated, operator-led execution.

1 Bain & Company, 2026 Global Private EquityReport https://www.bain.com/insights/topics/global-private-equity-report/

ZCG is a leading, privately held global firm comprised of private markets asset management, business consulting services, and technology development and solutions.

ZCG’s investors are some of the largest and most sophisticated global institutional investors including pension funds, endowments, foundations, sovereign wealth funds, central banks, and insurance companies.

For almost 30 years, ZCG Principals have invested tens of billions of dollars of capital. ZCG has a global team comprised of approximately 400 professionals. ZCG is headquartered in New York, with seven affiliated offices, across five countries. For more information on ZCG, please visit www.zcg.com.

You can also learn more about ZCGC, the business consulting services platform of ZCG, at www.zcgc.com, and explore ZCG’s technology affiliate, Haptiq, at www.haptiq.com.

ZCG Consulting (“ZCGC”) is the business consulting platform of ZCG and is a results‐oriented management consulting firm for middle market businesses. A reliable resource for private equity firms and their portfolio companies, our professionals offer deep functional expertise and customizable hands-on solutions to accelerate growth.

.png)

.png)